Owning a home is one of life’s greatest achievements, but a mortgage can feel like a long-term financial burden. What if you could pay off your mortgage in just five years? Accelerating your mortgage payoff is possible with careful planning, budgeting, and smart strategies. This guide explores how to pay off mortgage in 5 years, including practical tips, examples, and FAQs to help homeowners achieve financial freedom faster.

Why Paying Off Your Mortgage Early Matters

Paying off your mortgage early can have significant benefits:

- Interest Savings: You pay less interest over time, saving thousands or even tens of thousands of dollars.

- Financial Freedom: Eliminates one of your largest monthly expenses, freeing up cash for investments or lifestyle goals.

- Peace of Mind: Reduces debt stress and improves overall financial security.

- Equity Building: You own your home outright faster, giving you more flexibility in future financial decisions.

Understanding these benefits is the first step toward creating a plan to pay off mortgage in 5 years.

Step 1: Assess Your Current Mortgage Situation

Before accelerating payments, review your mortgage details:

- Principal Balance: How much you still owe.

- Interest Rate: Higher rates mean paying more interest over time.

- Loan Term: Original loan term (e.g., 30 years).

- Monthly Payment: Current monthly principal and interest.

Table 1: Mortgage Overview Example

| Item | Value ($) |

|---|---|

| Principal Balance | 300,000 |

| Interest Rate | 5% |

| Original Term | 30 years |

| Current Monthly Payment | 1,610 |

Knowing your starting point allows you to calculate how much extra you need to pay to achieve a 5-year payoff.

Step 2: Calculate Your Accelerated Payment

To pay off a mortgage in 5 years, you must make significantly higher monthly payments. The formula to calculate a monthly mortgage payment is:M=P×(1+r)n−1r(1+r)n

Where:

- M = Monthly payment

- P = Principal

- r = Monthly interest rate (annual ÷ 12)

- n = Total number of months (5 years × 12 = 60)

Example:

- Principal: $300,000

- Interest Rate: 5% annually → 0.004167 monthly

- Term: 5 years → 60 months

M=300,000×(1+0.004167)60−10.004167(1+0.004167)60≈5,660

You would need to pay roughly $5,660 per month to pay off the mortgage in 5 years, excluding taxes, insurance, or PMI.

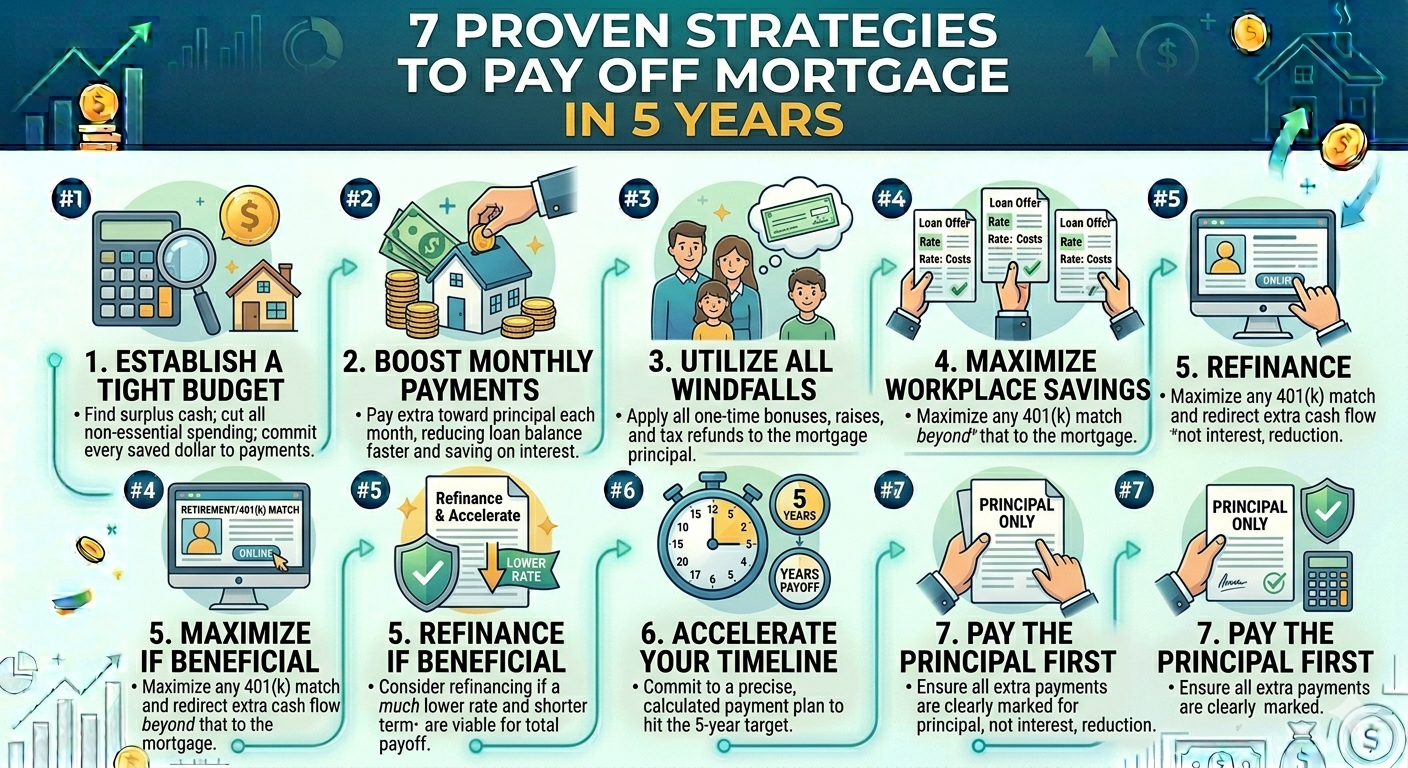

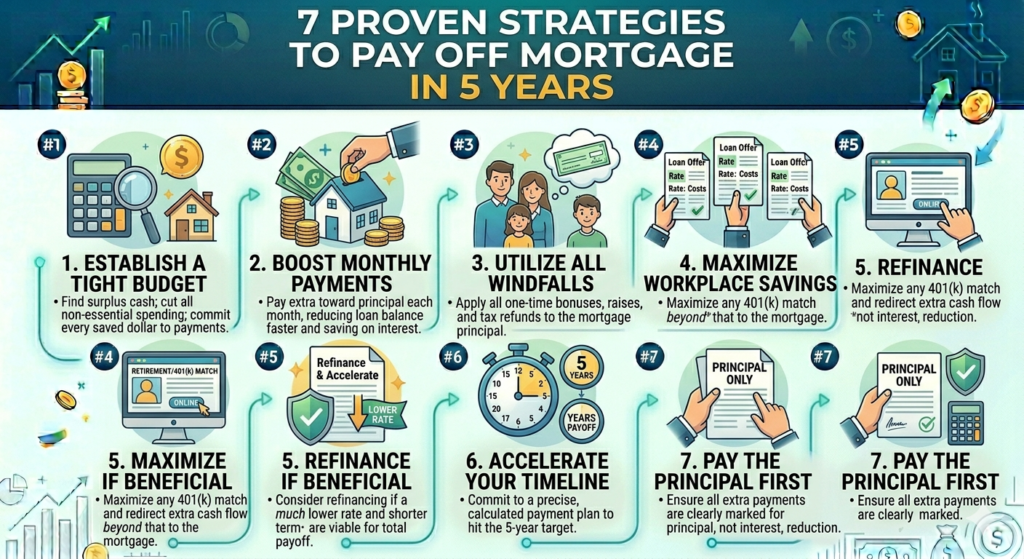

Step 3: Strategies to Pay Off Mortgage in 5 Years

Achieving this goal requires commitment and smart financial planning. Here are seven proven strategies:

1. Make Extra Principal Payments

Even small additional payments toward principal significantly reduce interest over time.

Table 2: Impact of Extra Monthly Principal Payments

| Extra Payment ($) | Months Saved | Interest Saved ($) |

|---|---|---|

| 500 | 6 | 14,200 |

| 1,000 | 12 | 27,500 |

| 2,000 | 24 | 55,000 |

2. Biweekly Payment Schedule

Instead of monthly payments, make half-payments every two weeks. This results in 26 half-payments or 13 full payments annually, effectively making an extra payment each year.

3. Refinance to a Shorter Term

Refinancing to a 5- or 10-year loan can lower interest rates and accelerate principal repayment. Ensure refinancing fees do not outweigh interest savings.

4. Reduce Expenses and Reallocate Savings

Cutting discretionary spending and redirecting the savings to mortgage payments accelerates your payoff.

Example Budget Reallocation:

| Expense Reduced ($/month) | Applied to Mortgage | Months Saved |

|---|---|---|

| Dining Out 500 | 500 | 10 |

| Subscription Services 100 | 100 | 2 |

| Travel Savings 300 | 300 | 6 |

5. Apply Bonuses and Windfalls

Use work bonuses, tax refunds, or inheritance money to make lump-sum payments toward your mortgage principal.

6. Increase Income Streams

Side gigs, freelance work, or rental income can provide extra funds for mortgage payoff.

7. Avoid New Debt

Avoid taking on new high-interest debt while accelerating your mortgage payments. Maintaining focus on the goal is key.

Step 4: Track Your Progress

Creating an amortization schedule helps visualize progress.

Table 3: Sample Amortization Snapshot (First 3 Months, Accelerated Payment)

| Month | Payment ($) | Principal ($) | Interest ($) | Remaining Balance ($) |

|---|---|---|---|---|

| 1 | 5,660 | 4,460 | 1,200 | 295,540 |

| 2 | 5,660 | 4,480 | 1,180 | 291,060 |

| 3 | 5,660 | 4,500 | 1,160 | 286,560 |

Tracking progress ensures you remain motivated and disciplined.

Step 5: Benefits of Paying Off Mortgage in 5 Years

- Interest Savings: Paying off early saves tens of thousands in interest.

- Financial Freedom: Eliminates a major monthly expense.

- Peace of Mind: Less debt stress.

- Investment Opportunities: Extra money can be used for investments or retirement savings.

Step 6: Challenges to Consider

- High Monthly Payment: Paying off mortgage in 5 years requires large monthly payments.

- Opportunity Cost: Extra funds could be invested elsewhere.

- Discipline Required: Avoid lifestyle inflation or new debts.

- Tax Implications: Mortgage interest deduction is lost sooner.

Step 7: Tools and Calculators

Using online mortgage calculators can simplify planning. Input:

- Loan balance

- Interest rate

- Accelerated term

- Extra payments

They will generate an amortization table showing interest savings and loan term reduction.

FAQs About Paying Off Mortgage in 5 Years

Q1: Can I really pay off mortgage in 5 years?

A: Yes, with larger monthly payments, extra principal contributions, and disciplined budgeting.

Q2: What percent of my salary should I allocate?

A: Depending on your income, 50–70% may be necessary for high balances, or smaller for lower mortgages.

Q3: Will I save a lot in interest?

A: Yes, accelerated payments drastically reduce total interest paid.

Q4: Is refinancing worth it?

A: Refinancing can help if the new interest rate is lower and fees are reasonable.

Q5: Can bonuses and windfalls help?

A: Absolutely, lump-sum payments toward principal significantly reduce loan term.

Q6: Are biweekly payments effective?

A: Yes, they create one extra full payment each year, reducing loan balance faster.

Q7: What if I can’t afford large payments?

A: Focus on extra payments when possible, use windfalls, or extend slightly longer than 5 years.

Q8: Will early payoff affect my credit?

A: Paying off early generally has a neutral or slightly positive impact on credit.

Q9: Are there penalties for early payoff?

A: Some lenders charge prepayment penalties. Check your mortgage agreement.

Q10: How do I track my progress?

A: Use amortization schedules or online calculators to monitor principal reduction.

Conclusion

Paying off your mortgage in 5 years is ambitious but achievable. With discipline, smart budgeting, extra payments, and possibly refinancing, you can eliminate your mortgage quickly, save on interest, and gain financial freedom. By following the seven strategies outlined above, tracking progress, and staying committed, paying off mortgage in 5 years can become a realistic goal.